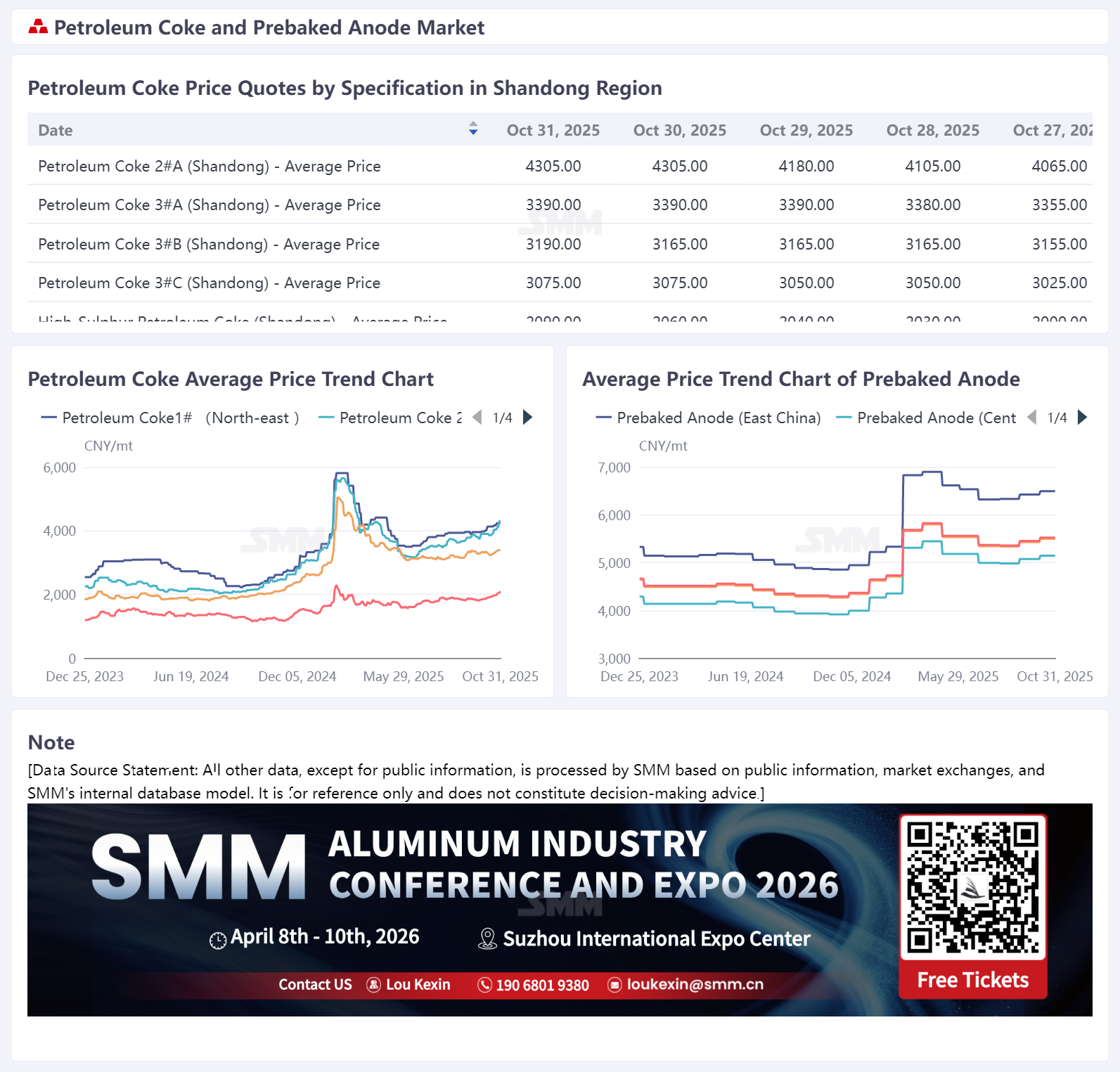

SMM October 31:

In October, SMM prebaked anode prices continued their upward trend. The procurement benchmark price for an aluminum plant in Shandong in October 2025 was 4,902 yuan/mt, up 1.45% MoM. According to SMM, prebaked anode export order prices mainly increased in October, with adjustments concentrated in the range of $10-20/mt. As of now, SMM anode prices in east China closed at 4,902-8,087 yuan/mt.

In the raw material market, petroleum coke and coal tar pitch showed divergent trends. In the petroleum coke market, low-sulphur petroleum coke performed particularly well: driven by active purchases from the anode materials market, refinery shipments remained generally healthy; more importantly, petroleum coke production at some refineries in north-east China declined, leading to market expectations of supply tightening. With multiple positive factors combined, low-sulphur petroleum coke prices continued to rise. According to SMM statistics, as of now, the average price of low-sulphur petroleum coke in north-east China was about 4,204 yuan/mt, up 3.62% from September 30, with further increases expected in early November. Due to strong purchasing enthusiasm from downstream carbon used in aluminum production and anode material enterprises, demand-side support remained firm. Major refineries raised petroleum coke prices multiple times, while local refinery prices also strengthened. Data show that, as of now, the SMM average price of petroleum coke from local refineries was 2,918 yuan/mt, up about 14.22% from September 30. In the coal tar pitch market, raw material coal tar prices fell during the month, leading to looser cost-side support, and coal tar pitch prices mainly declined. According to SMM data, as of now, the average price of coal tar pitch was 3,747 yuan/mt, down 3.60% from September 30. Overall, the sharp rise in petroleum coke provided solid support for prebaked anode costs.

Supply side, prebaked anode enterprises exhibited a mixed pattern of production increases and cuts this month. New projects in Yunnan, Guangxi, Inner Mongolia, Hunan, and other regions recently commenced operation one after another, bringing clear supply increments to the market. Meanwhile, several enterprises in Henan faced production constraints due to environmental protection-related controls, individual enterprises in north-west China saw output decline due to environmental factors, and some enterprises in other regions experienced production pullbacks due to equipment issues or maintenance. Overall, the output released from new project startups provided the main support, and domestic prebaked anode supply increased compared to the previous period.

Demand side, domestic operating aluminum capacity continues to remain high. Entering November 2025, winter environmental protection restrictions are expected to impact the operating rates of individual enterprises. However, considering that aluminum production cannot immediately drop to zero shortly after potline shutdowns, production changes are expected to be relatively small. Domestic demand for prebaked anodes remains favorable. Regarding export orders, based on September 2025 prebaked anode export data, China's prebaked anode exports reached 206,300 mt, up 11.90% YoY but down 1.06% MoM, indicating relatively small fluctuations from the previous month. Cumulative prebaked anode exports for 2025 totaled 1.6445 million mt, up 4.10% YoY. Specifically, orders exported to Canada, the UAE, Indonesia, and Germany showed significant increases, with increments exceeding 10,000 mt each, totaling over 57,600 mt. Conversely, orders to Malaysia, Spain, Iceland, and Saudi Arabia saw substantial declines, with decreases over 9,000 mt each, totaling approximately 48,100 mt. Price side, prebaked anode export prices increased in September, with the average export price up 19.40% YoY. Supported by rising domestic raw material costs, prebaked anode export prices continued an upward trend in October. Overall, current prebaked anode export orders show sufficient resilience, and the price uptrend remains solid.

Brief Comment: So far, an aluminum enterprise in Shandong has announced the November 2025 prebaked anode tender benchmark price, which rose by 222 yuan/mt MoM. Simultaneously, a major domestic prebaked anode sales company increased its sales price by 251 yuan/mt MoM. According to SMM data, as of October 31, China's comprehensive cost for prebaked anode increased to 5,125 yuan/mt, up 3.31% from September 30. The current raw material market is performing well, providing some support for prebaked anode prices. Particularly for petroleum coke, downstream demand is generally favorable, purchasing enthusiasm in the carbon industry is moderate, and demand from the anode material market for petroleum coke persists. Considering various factors, the price center for petroleum coke in November is expected to move higher. Against this backdrop, prebaked anode prices, directly supported by rising raw material costs, are expected to continue their upward trend.